For our Coolchecks.net customers, Richard Cox brings us advice about keeping more of our money.

One of the most often-discussed aspects of mutual funds is the fact that they tend to produce poor performances relative to the S&P 500 when things are judged on a pre-tax basis. And, in many cases, these comparisons become even less favorable when looking at mutual funds on an after-tax basis. Money managers tend to under-perform relative to Index funds because Index funds will hold investments for the long term. This becomes important when investors are looking to minimize the expenses that are created when stock investments are bought and then sold on a short-term basis.

When we look at the capital gains distributions in Index funds and compare these to those generated by money managers, significant lessons can be learned. These lessons essentially tell us that low turnover rates (a small number of trade transactions) and minimal cash balances (in funds that remain almost fully invested) can help investors to capture enhanced returns relative to other investment options.

Advantages of Index Funds

To be sure, index fund managers have an advantage that is not possessed by money managers. The S&P 500 500 index is constructed by the Standard & Poor’s editorial board, so all these fund managers need to do is look at the stock weightings in the S&P 500 and distribute the managed money according to those weightings. Selling stock holdings is an even easier process, as these index managers only need to sell shares when the makeup of the index is updated. Typically, the S&P 500 will see 10 to 15 stock changes each year, and these tend to come from bankruptcies, mergers, acquisitions, or heavy corporate distress. When we compare these changes to the number of “buys and sells” conducted yearly in the average mutual fund, 10 to 15 is a very small number.

If capital distributions that can be found in the Vanguard Index Trust 500 show 15 cents in short-term capital gains over a given year, 40 cents in long-term capital gains, and the Vanguard Index Trust 500 closes that year with a net asset value (NAV) of $90 per share, it becomes easy to see that the relatively low taxes (likely around 55 cents) do little to diminish the returns in either of these funds. It should also be remembered, however, that an investor would take on additional tax consequences if shares of the fund were sold.

Lowering Your Tax Liabilities by Keeping Your Money Invested

Most new investors, however, are looking to create wealth over larger time horizons and to use the benefits of compounding returns to their highest advantage. Looking at things on an after-tax basis, investors can create more value in their investments when keeping money invested (i.e. not cashing-in your shares). So, while paying high fees can diminish your returns, handing over money in taxes (for fund shares that didn’t need to be sold) can have the same negative effect.

As another example, assume that Vanguard’s Windsor fund creates short-term gain distributions of 85 cents and a long-term distribution equal to $2. If the fund possesses a NAV equal to $17 at the end of the year, Windsor will generate 6.5 times the tax burden (per share) while showing a NAV that is 81% lower. If Windsor creates returns of 20% for the year (and the S&P 500 generates returns of 30% for the same period), most of Windsor’s returns will be taxed as capital gains distributions. This can reduce those returns by as much as 15% to 35%. (Here the exact reduction will depend on the tax bracket of the investor.)

The troubling reality is that a majority of mutual fund providers choose not to highlight after-tax returns. They say that this is because individual tax situations are different, but if after-tax returns were highlighted, the performance differences between your typical mutual fund and in the S&P 500 would become much larger and more difficult to ignore. Another benefit gained when using a predetermined investment plan (which includes less frequent share sales) is that this reduces the amount of money you have stored in low yield cash holdings. It is possible for index funds to have more than 98% of its cash invested in market assets, but mutual funds will typically have much larger amounts of cash on hand (i.e. not actively invested). So if your money is in a mutual fund, and only 90% or your cash is invested, it becomes more difficult to beat the returns posted by the index fund because of the smaller amounts of money actively invested.

All of these factors create some combined negatives, because money managers must outperform the index so that they can make up for increased expenses and because they are never fully invested with all available cash resources. So, if money managers do beat the market (or simply break even) on a pre-tax basis, any value gains made for individual investors might be depleted with capital gains distributions which make a large percentage of these gains taxable.

Lessons for Individual Investors

So, when individual investors want to make their own financial decisions, the lessons here should be very clear: The best approach for generating larger, long-term returns is through maximizing money that is actively invested in the market and in adhering to the rules of tax efficiency. When the effects of taxation are calculated, outperformance margins that many short-term investors believe they have captured are significantly diminished.

Typically, the argument of these short term investors is that you will have to sell your shares at some point. But the reality shows us that when money compounds over longer time frames (as gains are reinvested, rather than cashed out), the lower tax rates for long-term shareholders create after-tax benefits that can be substantial. This does not even factor-in the possibility of owning stocks with dividend yields, which allow you to capture a rising income – gained through simple stock ownership. In some cases, it will be possible to live on your dividend income and leave your invested equity untouched (and without additional tax liabilities).

These are the reasons why S&P 500 Index investments are tough competition when compared to managed money accounts. When we understand why the S&P 500 index fund is often a preferable investment vehicle, it is possible to understand how to invest and keep expenses low. When investors minimize tax burdens and maximize the amount of money that is actively invested in the market, returns for the typical S&P 500 index fund far surpass those generated by professionally managed money. As an investor, your goal is to replicate this approach as closely as possible, as this will generate strong returns on an after-tax basis that are above and beyond what is typically seen in the market averages.

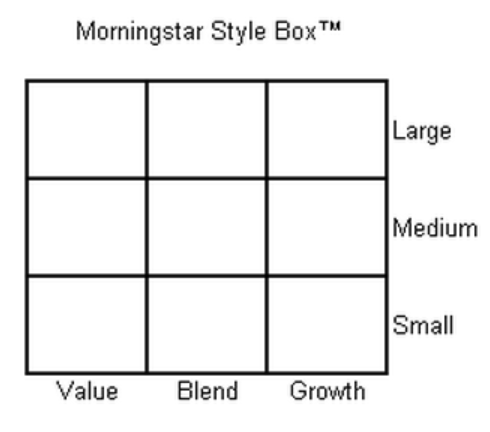

This configuration allows you to place your chosen fund its correct category (one box on the “tic tac toe” spectrum). This is helpful because it will allow you to compare total performance (rates of return) with funds of a similar size and investment approach. Typically, investors make these comparisons over 3, 5, and 10 year time horizons (allowing you to smooth out short term fluctuations in the market). Of course, performance comparisons can also be made relative to a benchmark index like the S&P 500, but the more specific performance comparisons (to those funds in a similar Morningstar category) tend to be more useful.

This configuration allows you to place your chosen fund its correct category (one box on the “tic tac toe” spectrum). This is helpful because it will allow you to compare total performance (rates of return) with funds of a similar size and investment approach. Typically, investors make these comparisons over 3, 5, and 10 year time horizons (allowing you to smooth out short term fluctuations in the market). Of course, performance comparisons can also be made relative to a benchmark index like the S&P 500, but the more specific performance comparisons (to those funds in a similar Morningstar category) tend to be more useful.